As 2025 approaches, homeownership remains a key aspiration for many individuals across India. With a broad range of home loan schemes available from various banks and financial institutions, prospective homeowners have a wide variety of options to choose from. This comprehensive guide explores the best home loan schemes for 2025, helping you make an informed decision based on interest rates, eligibility criteria, and loan tenures.

Whether you’re a first-time homebuyer or looking to refinance your existing loan, understanding these home loan schemes is essential to secure the best deal. Let’s dive into the top home loan options in India for 2025.

The State Bank of India (SBI) offers one of the most competitive home loan schemes in India, making it a preferred choice for many homebuyers.

HDFC Ltd is one of India’s leading housing finance companies, known for offering home loans with attractive features and flexible terms.

ICICI Bank provides flexible home loan schemes with low interest rates and convenient repayment options.

Axis Bank offers a wide range of home loan products designed for salaried individuals and self-employed professionals.

PNB Housing Finance is known for providing affordable and transparent home loan options to individuals across India.

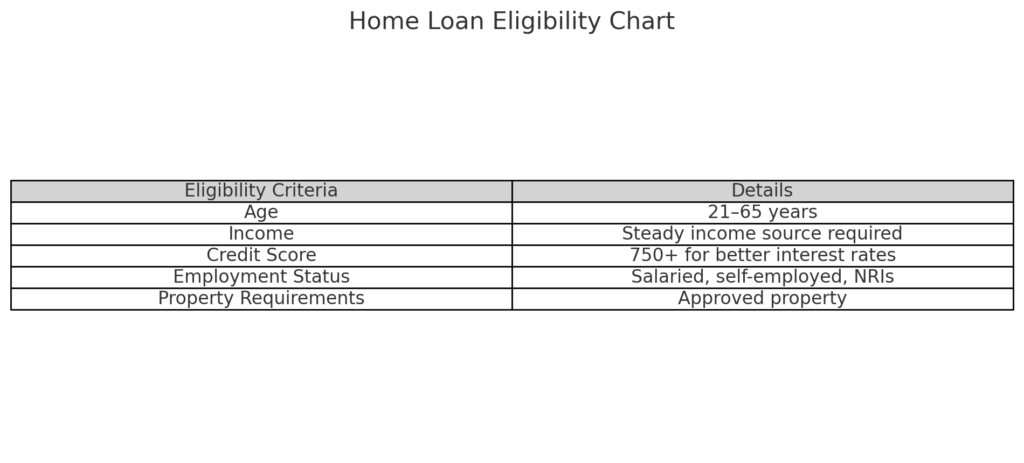

Eligibility for home loans in India depends on various factors, including your age, income, credit score, and employment status. Here’s a quick overview of the general eligibility criteria:

| Criteria | Details |

|---|---|

| Age | 21 to 65 years (for salaried individuals) |

| Income | Regular, steady income from a recognized source |

| Credit Score | Preferably 750 or above (higher scores secure better rates) |

| Employment Status | Salaried, self-employed, business owners, or NRIs |

| Property Value | Must meet the lender’s valuation standards |

The interest rate directly impacts your monthly EMI and the total cost of the loan. Look for lowest interest rates and understand whether the rate is fixed or floating.

Always compare the processing fees charged by different lenders. These fees typically range from 0.5% to 1% of the loan amount.

A longer tenure reduces your monthly EMI but results in higher overall interest payments. Choose a tenure that balances affordability and total cost.

Check the lender’s policy regarding prepayment and foreclosure. Some lenders charge penalties for early repayment, while others offer flexibility.

Ensure the lender offers an amount that is adequate to cover your property’s price, including registration and stamp duty costs.

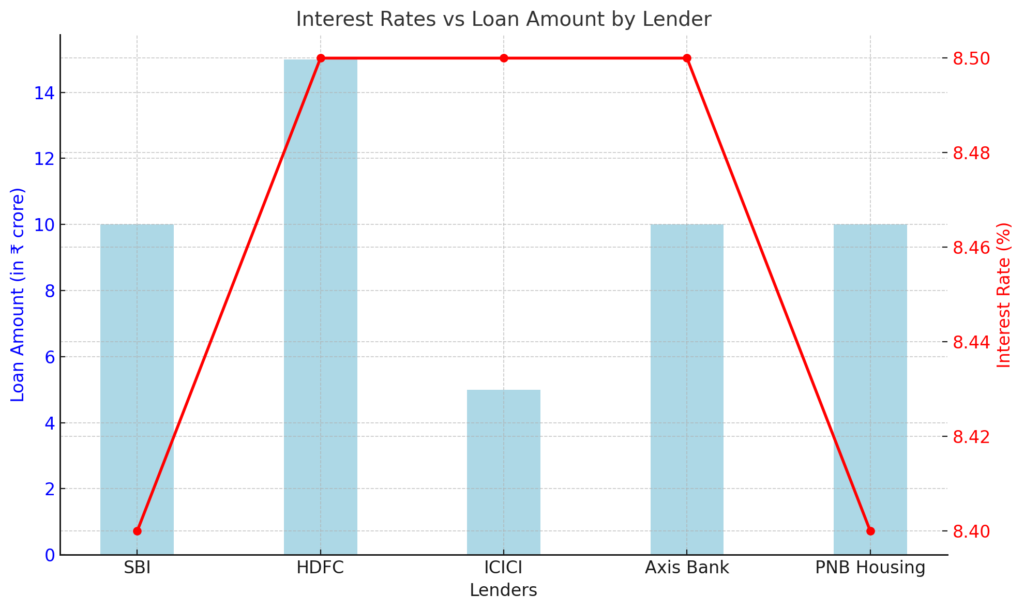

| Lender | Interest Rate (Starting) | Loan Amount | Processing Fee | Tenure (Max.) | Eligibility |

|---|---|---|---|---|---|

| SBI | 8.40% p.a. | Up to ₹10 crore | 0.35% (min ₹10,000) | 30 years | Salaried, self-employed, business owners |

| HDFC | 8.50% p.a. | Up to ₹15 crore | 0.50% (min ₹3,000) | 30 years | Indian residents, NRIs |

| ICICI | 8.50% p.a. | Up to ₹5 crore | ₹3,000 – ₹10,000 | 30 years | Salaried, self-employed, NRIs |

| Axis Bank | 8.50% p.a. | Up to ₹10 crore | 1% of loan amount | 30 years | Salaried, self-employed, NRIs |

| PNB Housing | 8.40% p.a. | Up to ₹10 crore | 0.50% | 30 years | Salaried, self-employed, NRIs |

Answer: To qualify for a home loan in India, applicants typically need to be between 21 to 65 years old, have a steady source of income, a credit score of 750 or above, and meet other lender-specific criteria. Eligibility also depends on employment status, income, and property value.

Answer: Common documents required for a home loan application include:

Answer: While a high credit score (750+) improves your chances of getting a home loan with favorable terms, it’s still possible to get a loan with a lower credit score. However, you may face higher interest rates or a lower loan amount. It’s advisable to improve your credit score before applying for a loan.

Answer: A fixed interest rate remains the same throughout the loan tenure, offering stable EMIs. A floating interest rate varies with market conditions, which means your EMIs could increase or decrease based on changes in interest rates.

Answer: The home loan amount you can get is typically based on your monthly income and credit score. Lenders usually offer 60% to 80% of the property value as a loan, and the EMI should not exceed 40% to 50% of your monthly income.

Choosing the right home loan is crucial to making your dream of homeownership a reality. In 2025, the State Bank of India (SBI), HDFC Ltd, ICICI Bank, Axis Bank, and PNB Housing Finance offer some of the best home loan schemes, each catering to different needs and financial situations. Whether you’re looking for low-interest rates, flexible tenures, or competitive processing fees, these schemes are designed to meet a variety of requirements.

Before applying for a home loan, make sure to compare interest rates, check eligibility based on your income and credit score, and understand the processing fees, prepayment charges, and other terms to make an informed decision.

If you are unsure about which scheme suits your needs, consider speaking with a financial advisor or loan expert who can help guide you through the process and ensure that you choose the most beneficial option for your home loan.

For personalized advice or to apply for one of the best home loan schemes for 2025, feel free to contact us or explore the loan options mentioned above.

Part of the NCR Guide editorial team, covering news, real estate, food and lifestyle across Delhi NCR.

Join thousands of Delhi NCR residents who start their day with our morning brief — top stories, real estate updates, events and deals.