Buying a home is one of the most significant financial decisions of your life, and choosing the right home loan can make a world of difference in how smoothly the process goes. With numerous home loan providers offering a variety of schemes, it can be overwhelming to choose the best one. But with a little bit of knowledge and a careful approach, you can secure the best home loan deal for your needs.

This article offers expert tips to help you find the best home loan deal for 2025, from understanding the factors that affect your loan to negotiating with lenders for better terms.

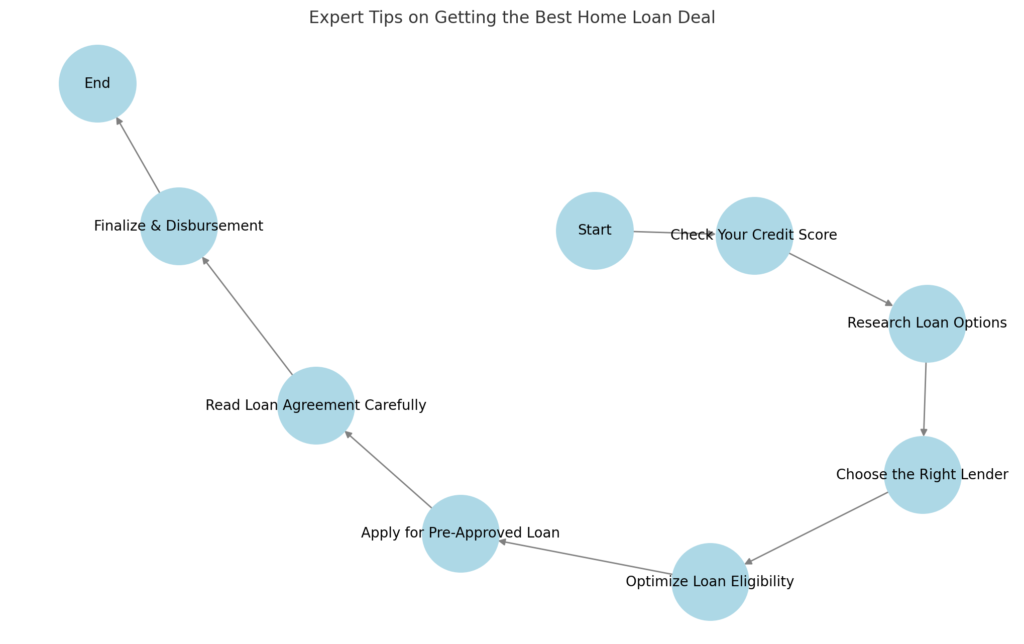

Your credit score plays a crucial role in determining the interest rate on your home loan. Lenders use your credit score to assess your creditworthiness and decide how risky it is to lend to you. A higher score means you are more likely to get a loan at favorable terms.

Before applying for a loan, check your credit score through online tools or credit bureaus (such as CIBIL, Experian, or Equifax). If your score is lower than 750, consider improving it by clearing any outstanding debts or correcting any errors in your credit report.

One of the biggest mistakes homebuyers make is settling for the first home loan offer they receive. Each lender has different terms, interest rates, processing fees, and eligibility criteria. By comparing multiple lenders, you can ensure you’re getting the best deal.

Use online comparison tools to quickly compare interest rates, processing fees, and other charges across different lenders.

In India, home loans typically come with either fixed or floating interest rates, and understanding the difference is key to getting the best deal.

If you are opting for a floating rate, check if your lender offers a cap on the rate, ensuring your interest doesn’t rise beyond a certain level.

Before applying for a home loan, use eligibility calculators provided by lenders or financial websites. These calculators determine how much loan you can afford based on your monthly income, existing debts, credit score, and age.

Be honest when entering your income and expenses. If your eligibility is lower than expected, consider adjusting your loan amount or choosing a longer tenure.

While it’s tempting to buy the biggest home you can afford, remember that a home loan is a long-term financial commitment. Ensure that your monthly EMI fits comfortably within your budget. A general rule of thumb is to keep your EMI at or below 40%-50% of your monthly income.

Calculate the EMI using an online EMI calculator before applying. Consider future expenses such as children’s education, healthcare, and other investments before deciding on the loan amount.

Many borrowers don’t realize they can negotiate the terms of their home loan. While the interest rate might not be flexible in all cases, you can still negotiate other factors, such as processing fees, prepayment options, and even the loan amount.

Once you’ve compared offers from different lenders, approach your preferred lender with the terms from others. Lenders may be willing to match or beat competitors’ offers to secure your business.

The Indian government offers various schemes, such as the Pradhan Mantri Awas Yojana (PMAY), which provides subsidies on home loans for eligible borrowers. These schemes are especially beneficial for first-time homebuyers and low-income individuals.

Check if you qualify for any government schemes before finalizing your loan. The subsidy can significantly reduce your EMI burden.

Interest rates are not fixed and can fluctuate due to various economic factors. Once you’ve identified the best interest rate, try to lock in that rate for as long as possible to avoid sudden increases.

Many lenders offer a rate lock-in option for up to 6 months. If you find a favorable rate, locking it in early can prevent you from paying higher rates if the market rates rise.

To avoid delays in loan approval, ensure all the required documents are ready before applying. Typically, these documents include:

Ensure all documents are up to date and free of errors. Any discrepancies in your paperwork can lead to delays or rejection.

Before signing the agreement, thoroughly review the loan agreement to understand all the terms and conditions. Pay attention to:

Ask your lender to explain any terms you don’t understand, especially when it comes to fees, charges, or penalties.

Answer: To qualify for a home loan in India, applicants typically need to be between 21 to 65 years old, have a steady source of income, a credit score of 750 or above, and meet other lender-specific criteria. Eligibility also depends on employment status, income, and property value.

Answer: Common documents required for a home loan application include:

Answer: While a high credit score (750+) improves your chances of getting a home loan with favorable terms, it’s still possible to get a loan with a lower credit score. However, you may face higher interest rates or a lower loan amount. It’s advisable to improve your credit score before applying for a loan.

Answer: A fixed interest rate remains the same throughout the loan tenure, offering stability. A floating interest rate fluctuates based on market conditions, which means your EMIs could change over time.

Answer: The home loan amount you can get is typically based on your monthly income and credit score. Lenders usually offer 60% to 80% of the

Part of the NCR Guide editorial team, covering news, real estate, food and lifestyle across Delhi NCR.

Join thousands of Delhi NCR residents who start their day with our morning brief — top stories, real estate updates, events and deals.