Delhi NCR (National Capital Region) is one of India’s most dynamic real estate markets, encompassing Delhi, Noida, Gurgaon, Ghaziabad, and Faridabad. Whether to rent or buy property in this region in 2025 depends on multiple factors, including property prices, rental yields, economic conditions, job prospects, and lifestyle preferences. Making an informed decision requires a deep dive into financial comparisons, market trends, and personal circumstances.

Market Trends in 2025

A. Property Prices in 2025

Delhi NCR’s real estate prices have shown steady growth, with key areas like Gurgaon and Noida experiencing 5-10% price appreciation annually.

High-end localities such as Golf Course Road (Gurgaon), Greater Kailash (Delhi), and Jaypee Greens (Noida) continue to command premium prices, making homeownership a major financial decision.

Affordable housing segments in Ghaziabad and Faridabad are attracting middle-income buyers looking for long-term property appreciation.

Major infrastructure projects like Jewar Airport, Delhi-Mumbai Expressway, and expanded metro connectivity are influencing property prices, with some locations seeing a surge in investment potential.

Areas near IT and corporate hubs such as Cyber City Gurgaon, Noida Expressway, and Dwarka Expressway have seen increased demand due to better job opportunities and business growth.

B. Rental Market Trends

Rental rates have increased significantly in 2024-25, particularly in business hubs like Cyber City, Gurgaon and Sector 150, Noida, where corporate expansion is driving housing demand.

Average rental yields (annual rent as a percentage of property price) in Gurgaon and Noida range between 2.5% to 3.5%, making renting an attractive option for those prioritizing financial flexibility.

Delhi’s prime locations, such as South Delhi and Connaught Place, have higher rental costs, while emerging suburbs offer affordable alternatives.

Co-living and serviced apartments are gaining popularity among young professionals, offering affordable yet convenient housing options.

The rental market is expected to remain strong, driven by a growing workforce, increased urban migration, and demand for flexible living arrangements.

Financial Comparison: Buying vs. Renting

One of the most crucial aspects of deciding whether to rent or buy a property in Delhi NCR is understanding the financial implications of both choices. Buying a property comes with a significant initial investment, including down payments, home loan EMIs, taxes, and maintenance costs. Renting, on the other hand, offers flexibility with lower upfront costs and predictable monthly expenses. Below is a breakdown of the financial differences between renting and buying in Delhi NCR.

Renting vs. Buying Comparison

Factor

Renting in Delhi NCR

Buying in Delhi NCR

Upfront Cost

1-2 months security deposit

20% down payment + taxes

Monthly Expense

Fixed rent

EMI + maintenance charges

Flexibility

Easy to relocate

Long-term financial commitment

Equity Building

No ownership

Builds asset over time

Tax Benefits

None

Tax deductions on home loans

A. Cost of Buying a Property in Delhi NCR

Buying property in Delhi NCR requires a substantial investment, especially in premium locations. While homeownership builds equity over time, it also involves high upfront costs and ongoing expenses such as property taxes, loan repayments, and maintenance charges. Here’s an estimate of property prices in different areas of Delhi NCR:

Location

Average Property Price (Per Sq. Ft.)

2BHK Price (Approx.)

Gurgaon

₹10,000 – ₹25,000

₹80 Lakh – ₹2 Cr

Noida

₹6,500 – ₹15,000

₹60 Lakh – ₹1.5 Cr

Delhi

₹15,000 – ₹40,000

₹1.2 Cr – ₹3.5 Cr

Ghaziabad

₹4,500 – ₹8,000

₹40 Lakh – ₹80 Lakh

Faridabad

₹3,500 – ₹7,000

₹35 Lakh – ₹70 Lakh

B. Cost of Renting a Property in Delhi NCR

Renting offers more financial flexibility as it requires no major upfront investment apart from security deposits and monthly rent. It also eliminates long-term financial liabilities such as home loan repayments. Below is an estimate of monthly rental costs for a 2BHK apartment in different parts of Delhi NCR:

Location

Average Monthly Rent (2BHK)

Gurgaon

₹35,000 – ₹70,000

Noida

₹25,000 – ₹50,000

Delhi

₹40,000 – ₹90,000

Ghaziabad

₹15,000 – ₹30,000

Faridabad

₹12,000 – ₹25,000

C. Additional Costs to Consider

Beyond the purchase price or rental costs, there are several other expenses that buyers and renters should factor into their decision:

Home Loan EMI: If purchasing a property, expect to pay ₹50,000 – ₹1.5 Lakh per month (for a ₹1 Cr loan at 8.5% interest), making it a long-term financial commitment.

Maintenance Charges: Homeowners in gated communities must pay ₹2,000 – ₹15,000 per month for building upkeep, security, and amenities.

Stamp Duty & Registration Fees: Buying property also incurs legal costs, usually ranging between 5-7% of the total property value.

Property Tax: Homeowners must pay annual property taxes ranging between 1-2% of the property’s market value.

Insurance & Security Costs: Additional expenses for homeowners covering property insurance and gated community security fees can add to the long-term cost.

While owning property ensures asset appreciation over time, it also requires high initial and ongoing costs. Renting, on the other hand, provides the advantage of low initial investment and hassle-free living, making it an attractive option for those who prioritize financial flexibility and mobility.

Example Scenarios: Renting vs. Buying

Scenario 1: Young IT Professional in Gurgaon

Profile: Rahul, 28, earns ₹1.5 lakh/month, working in Cyber City, Gurgaon.

Decision: He prefers renting a 2BHK in DLF Phase 3 at ₹45,000/month rather than buying a ₹1.2 Cr property with ₹1 Lakh EMI.

Why? Renting allows flexibility, no debt burden, and easy relocation for career growth. He invests his savings in mutual funds and stocks for better liquidity.

Scenario 2: Family Looking for Stability in Noida

Profile: Priya and Amit, both in their 30s, have a child and stable jobs, earning ₹3 Lakh/month combined.

Decision: They buy a ₹1.5 Cr apartment in Sector 150, Noida, paying ₹1.2 Lakh EMI.

Why? Long-term investment, stability, and appreciation potential make buying a smarter choice. Their EMI is comparable to renting, so they build equity instead of paying rent.

Profile: Mr. Sharma, 60, with a pension of ₹1.2 Lakh/month, is unsure whether to buy or rent.

Decision: He buys a ₹70 Lakh property in Indirapuram, Ghaziabad, with savings.

Why? No EMI burden, passive rental income in the future, and security in old age. Buying ensures he doesn’t have to worry about rising rent in retirement.

Scenario 4: Startup Entrepreneur in Noida

Profile: Arjun, 32, has launched a tech startup in Noida and earns a fluctuating income. Decision: He chooses to rent a 2BHK in Noida’s Sector 62 for ₹30,000/month instead of buying a ₹1 Cr apartment. Why? Renting provides financial flexibility, allowing him to reinvest capital into his business rather than committing to home loan EMIs.

Scenario 5: NRI Planning to Settle in India (Delhi NCR)

Profile: Meera, 45, works in the U.S. and is planning to return to India in 3-5 years. Decision: She buys a ₹1.8 Cr apartment in Gurgaon’s Golf Course Extension Road while continuing to live abroad. Why? Property appreciation and rental income make it a smart investment. She rents it out for ₹75,000/month until she moves back.

Scenario 6: Government Employee with a Stable Job in Delhi

Profile: Sunil, 50, is a government employee with a steady pension plan. Decision: He buys a ₹90 Lakh property in Dwarka, Delhi with minimal home loan assistance. Why? Stability, long-term security, and potential future rental income make homeownership a better choice for him.

Scenario 7: Frequent Traveler Working in Multiple Cities

Profile: Riya, 29, works in corporate consulting and shifts locations every 2-3 years. Decision: She rents a fully furnished apartment in Gurgaon for ₹50,000/month instead of buying. Why? Renting allows her to live close to work, avoid long-term financial commitment, and relocate easily when needed.

Key Takeaways: Should You Rent or Buy in Delhi NCR in 2025?

Renting is better if: You need flexibility, have a short-term stay, or want to avoid financial burden.

Buying is better if: You seek stability, long-term investment, and tax benefits.

For investors: Buying property in developing areas can offer better returns in the long run.

For working professionals: Renting allows mobility and better financial management without EMI stress.

For families and retirees: Buying ensures stability and asset creation, making it a preferred choice.

Ultimately, the decision depends on personal financial goals, job stability, and lifestyle preferences. Evaluate both options carefully before making a commitment.

FAQs: Renting vs. Buying Property in Delhi NCR

1. Is it cheaper to rent or buy a home in Delhi NCR in 2025?

It depends on factors like location, loan interest rates, and your financial goals. Renting is cheaper in the short term, as it eliminates home loan EMIs, property taxes, and maintenance costs. However, buying a home is beneficial in the long run, especially in high-growth areas where property values are appreciating.

2. How much should I earn to afford a house in Gurgaon or Noida?

To comfortably buy a ₹1 Cr property with a 20% down payment, your monthly income should ideally be ₹2-3 Lakh. This ensures your EMI (₹80,000 – ₹1.2 Lakh/month) does not exceed 40-50% of your income. Renting requires a lower financial commitment, with good 2BHK options available for ₹30,000 – ₹60,000/month.

3. What are the hidden costs of buying property in Delhi NCR?

Buying property comes with extra costs beyond the purchase price:

Stamp Duty & Registration Fees (5-7% of property value)

Home Loan Interest (8-9% annually)

Property Tax (1-2% annually)

Society Maintenance Charges (₹2,000 – ₹15,000/month)

Renovation & Furnishing Costs (₹5 Lakh – ₹20 Lakh, depending on property size and quality)

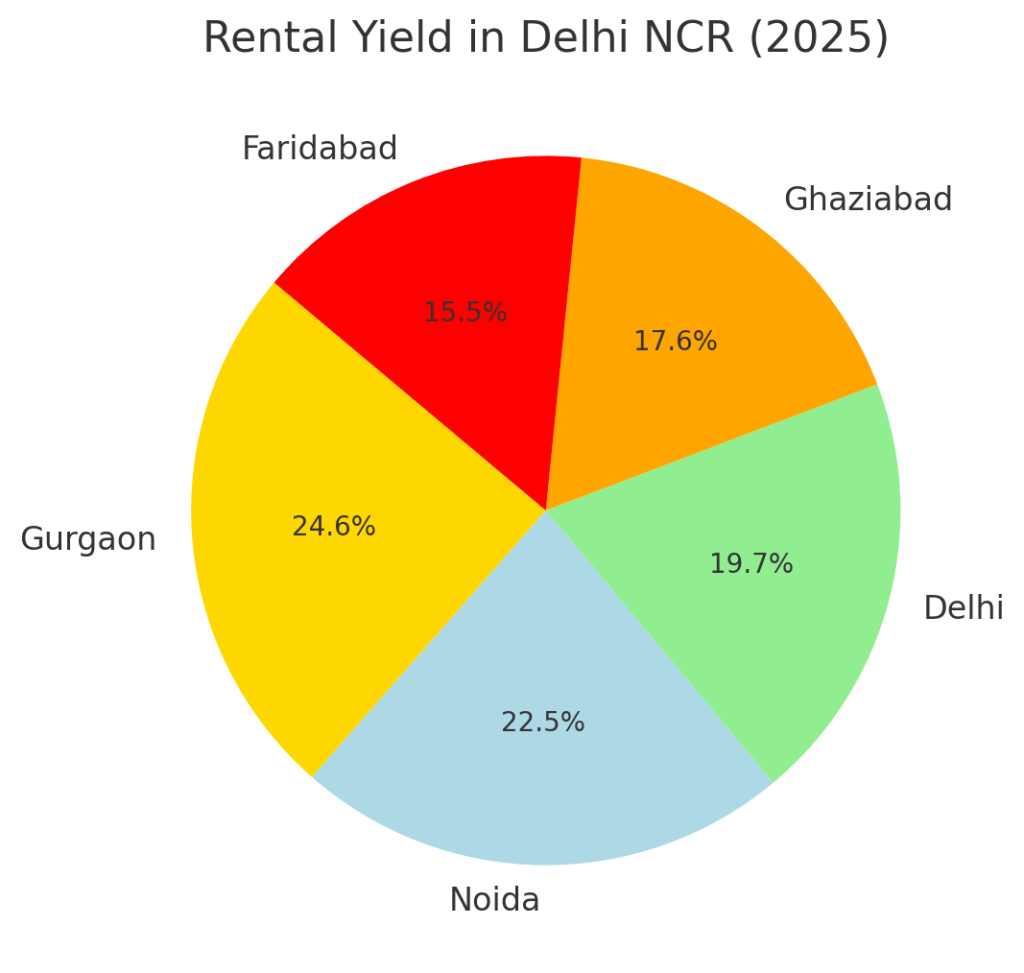

4. Which areas in Delhi NCR have the highest rental yield?

The best areas for rental investment with high rental yields (2.5% – 4%) are:

5. Is buying property in Noida or Gurgaon better for investment?

Gurgaon: Higher appreciation rates, better luxury housing, and corporate hubs like Cyber City & Golf Course Road. Ideal for high-budget investors.

Noida: More affordable, well-planned infrastructure, upcoming Jewar Airport boost, and lower property prices compared to Gurgaon. Ideal for mid-range investors.

6. How much should I save before buying a house in Delhi NCR?

To buy a ₹1 Cr property, you need at least ₹25-30 Lakh in savings for:

Down Payment (20%) – ₹20 Lakh

Stamp Duty & Registration Fees – ₹5-7 Lakh

Initial Maintenance & Furnishing – ₹5 Lakh+

7. What percentage of my income should go towards rent in Delhi NCR?

Ideally, your rent should not exceed 30-35% of your monthly income. For example:

If you earn ₹1.5 Lakh/month, keep rent under ₹45,000-₹50,000.

If you earn ₹80,000/month, aim for rent under ₹25,000-₹30,000.

8. Are there any tax benefits to buying property in Delhi NCR?

Yes, homeowners can claim tax benefits:

Section 80C: Deduction up to ₹1.5 Lakh on principal repayment.

Section 24(b): Deduction up to ₹2 Lakh on home loan interest.

Section 80EEA: Extra deduction of ₹1.5 Lakh for first-time buyers.

9. Should I buy a ready-to-move property or an under-construction home?

Ready-to-move homes: No waiting period, no GST, and immediate rental income if investing.

Under-construction homes: Usually 15-20% cheaper, but come with risks like delays and GST (5%).

10. Is it better to invest in a flat or a plot in Delhi NCR?

Flats: Easier to resell, generate rental income, and have modern amenities. Best for short-term and mid-range investments.

Plots: Offer higher appreciation over time but require long-term holding and additional construction costs. Best for investors looking for long-term capital gains.

11. What are the best locations for budget home buyers in Delhi NCR?

For buyers looking under ₹60 Lakh, the best locations are:

Yes, negotiation is common, especially for under-construction properties. You can negotiate:

Base price (5-10% discount) depending on market conditions.

Additional charges (parking, club membership, maintenance fees).

Payment plans & interest rates with developers and banks.

13. How does renting affect credit score compared to buying a house?

Renting does not impact your credit score, as rent payments are not reported to credit bureaus in India.

Buying a house with a home loan improves credit score if EMI payments are made on time.

14. How do I decide if I should rent or buy based on my stay duration?

If staying less than 5-7 years, renting is better as transaction costs (stamp duty, loan interest) are high for short-term ownership.

If staying 10+ years, buying is better as EMIs convert into asset ownership.

15. What are the risks of buying property in Delhi NCR?

Builder delays: Always check RERA registration before investing in under-construction properties.

Legal issues: Verify land titles and property approvals to avoid disputes.

Resale market fluctuations: Some locations see slow resale demand, affecting liquidity.

16. What are the best government schemes for homebuyers in Delhi NCR?

Pradhan Mantri Awas Yojana (PMAY): Interest subsidy up to ₹2.67 Lakh for first-time buyers.

Delhi Development Authority (DDA) Housing Scheme: Affordable flats in select areas.

UP & Haryana Affordable Housing Schemes: Available for Noida and Gurgaon residents.

17. Is co-living or PG a better option than renting a flat?

For bachelors & working professionals, co-living or PGs are better as they offer lower costs (₹8,000-₹20,000/month), furnished spaces, and no maintenance hassle.

For families & long-term stays, renting a flat is better for privacy and space.

18. What are the major real estate trends in Delhi NCR for 2025?

Rise in hybrid work-friendly homes with dedicated office spaces.

Increased investment in Noida due to Jewar Airport.